I don’t know anyone who claims to enjoy a Colonoscopy, the preparation and the procedure are not things that are my fun list. There is no doubt that a Colonoscopy can help detect colorectal cancer. Starting at 50, the American Cancer Society recommends you begin regular colorectal cancer screening. More than 9 out of 10 diagnoses of colorectal cancer occur in patients at least 50 years old.

Due to new technology, we now have another option to detect colorectal cancer. Exact Sciences Corporation (EXAS) released their Cologuard DNA test kit this year. Cologuard is an easy to use, noninvasive colon cancer screening test based on the latest advances in DNA science. Cologuard finds both cancer and precancer situations. You can perform this test from their kit in the privacy of your own house and send the results to their lab for evaluation. Cologuard requires a doctor’s prescription and most doctors are just now coming up to speed on the benefits of this test. Centers for Medicare and Medicaid Services (CMS) have approved payment for this test in 2015, other insurance carriers should be jumping on this bandwagon. Traditional Medicare (Part B) patients should not have any co-pays, deductible amounts, or co-insurance for Cologuard. Medicare Advantage patients might be subject to laboratory co-pays or co-insurance as determined by their plan.

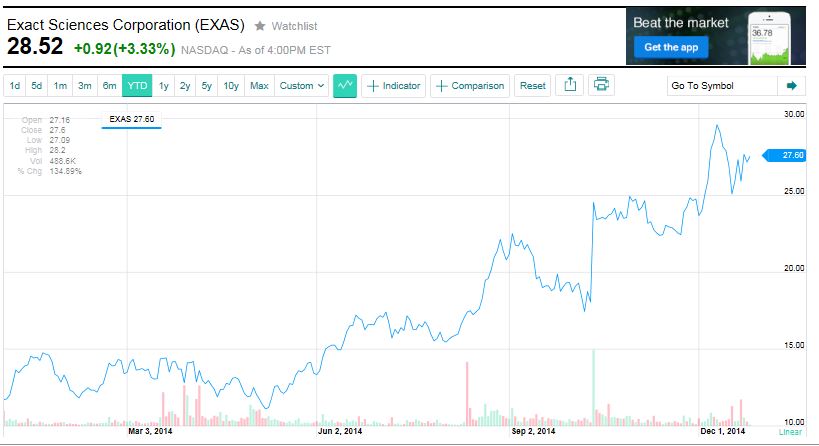

Now for the stock. Exact Sciences Corporation (EXAS) has already been up over 130% this year as compared to 18% for the S&P500. I started buying this stock in early summer in the $12-$15 range, it closed Friday at $28.52. Of 14 analysts who follow the stock, 4 rate it a Strong Buy, 6 a Buy, 3 a Hold and 1 an Underperform. EXAC is a somewhat volatile stock with a 1.48 beta.

I like buying stocks with a real life benefit and a great revenue growth story. This could easily double again in 2015 as the new Cologuard test kits get used by millions of people and the company starts to expand internationally.