You see all the talking heads on TV, explaining how they are long xxx stock and short xxx stock. They toss out complicated terms like forward EPS, tangible book value and so forth. Many have analysts on the payroll to help them pick the very best investments. Yet in 2014 about 80% of Hedge Funds are reportedly underperforming the overall all US market, namely the S&P 500 index (SPY). SPY is an ETF sold by State Street Advisors that is commonly referred to as the “market”.

Just to clarify a common misconception, many investors think the Dow Jones Industrial Averages “the Dow” is “the market”. It isn’t predominately because it is a very small sampling of 30 very large companies. In addition it is know as a “price weighted” average. This means that a 1% change in a $100 stock has twice the imp[act as a 1% change in a $50 stock. Therefore, if IBM at $155 and Visa at $258 have bad days the Dow average will be down sharply, but the overall market could be up nicely.

Today it is really easy to have a “market performing” investment portfolio, just buy the market. Arguably the great investor of all time, Warren Buffet suggests that people who don’t want to take the time to actively manage a portfolio just buy the S&P 500 Index. The S&P 500 Index is actually 501 stocks, and 500 companies. It just so happens that Google is listed twice due to a split into type types of shares for the same company (voting and non-voting).

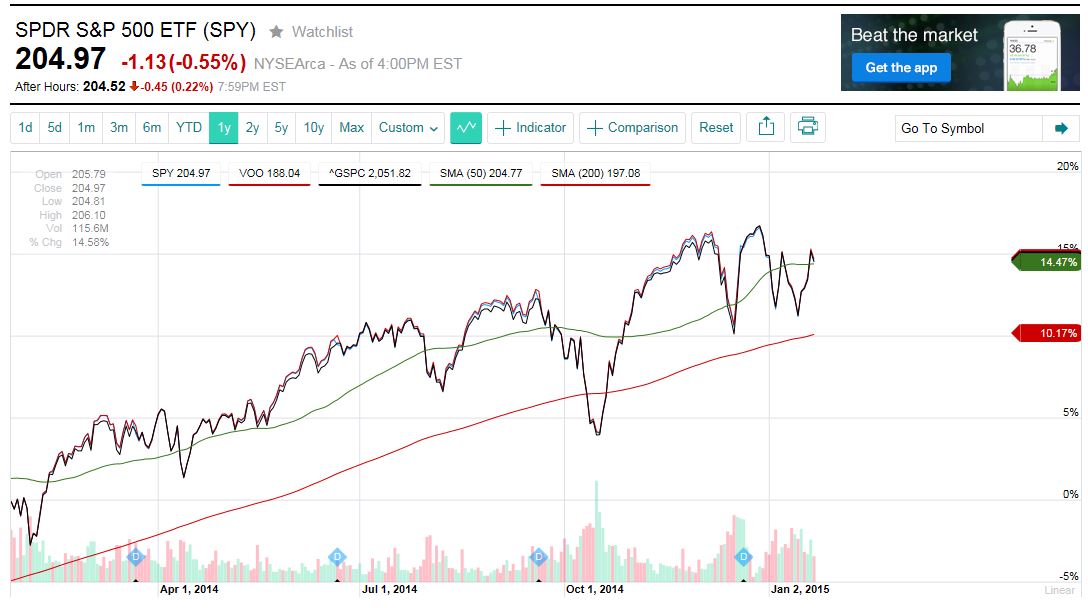

If you put all of your investments in just the SPY ETF or the Vanguard S&P Index ETF “VOO” you would have made over 14% in the last 12 months. In addition you would have collected 1.9% in dividends.

You can choose either fund, it just so happens that VOO has a smaller annual expense fee of 0.05% vs. the SPY at 0.09% expense ratio. If you had a $1,000,000 investment the SPY ETF would costs you $400/year more in fees than the VOO.

If you want to beat the Hedge Funds and most other investment managers, it is simple, just invest in the “market”.