The stock market has been very volatile for the last 6-9 months. So, what is a nice safe investment to add to your portfolio?

As I wrote in a previous blog posting, “This Stock has been flat for 3 years – You’ll just love it!” preferred stocks can generate a very nice yield and still have a margin of safety.

Most investors don’t understand preferred stocks. Preferred stocks are positioned between common stocks and bonds. Most commonly preferred shares carry no voting rights but have a higher claim to earnings than common share and are usually less volatile than common. When the S&P 500 fell 37% in 2008, for example, the iShares preferred fund fell only 24%. Preferred shares are next in line to bond holders in the capital chain of any company. Investors can easily choose from preferred stock ETF’s or individual stocks.

I happen to like the safety of bank preferred stocks.

Here are my favorite preferred stocks:

- Ladenburg Thalmann Financial Services (LTS-PA) 9.75% yield

- Barclays Bank (BCS-PD) 7.7% yield

- Wells Fargo (WFC-PL) 7.5% yield, AND a convertible option

Please note that most preferred shares are lightly traded and the best thing to do is to enter a limit order with your price and let the order come to you.

By allocating a portion of your portfolio to some of these high-yielding investments you’ll be able to improve your cash flow while waiting for the next Facebook or Apple investment to come along. In future posts we’ll discuss the pros and cons of these investments and some helpful tips.

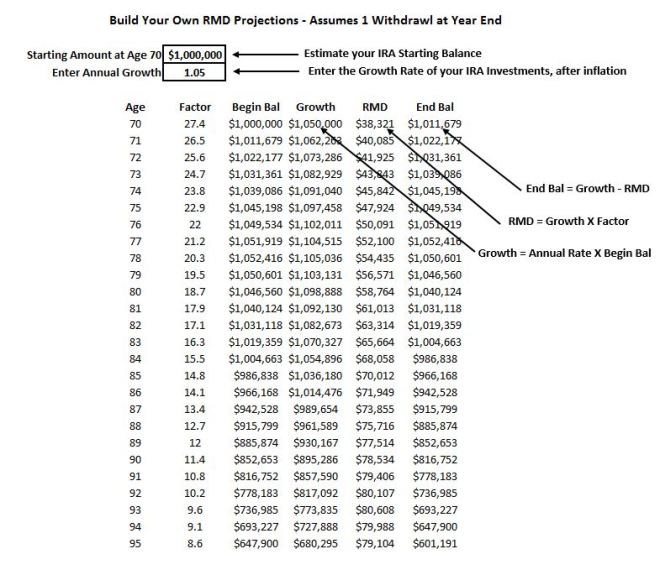

We are all faced with the dilemma of taking Required Minimum Distribution from our IRA accounts when we turn 70 years old. If you have accumulated large IRA’s (including transferred 401K accounts), this can be a problem.

We are all faced with the dilemma of taking Required Minimum Distribution from our IRA accounts when we turn 70 years old. If you have accumulated large IRA’s (including transferred 401K accounts), this can be a problem.