Summary

- An annuity can provide a steady stream of reliable income during retirement

- You can build your own annuity with benefits not available elsewhere

- Dividends completely cover my Required Minimum Distributions and the principle continues to grow

- Commercial annuities invest if the same types stocks and bonds you can purchase

- Commercial annuities have substantial fees, end of life limitations and no return of capital

- My investments include a taxable account, ROTH IRA and a IRA. This article covers my IRA “annuity”

What is an Annuity

An annuity is an insurance contract issued by financial institutions (usually an insurance company) with the idea of you providing a large cash amount up front, the institution investing the money and then paying out invested funds in a fixed income stream in the future for life.

Annuity Shortcomings

The general bet is that you will get more out than what you contributed up front and won’t outlive your money. Annuities can be very complex and few people buying them really understand all of the fine print. An annuity contract can be a small booklet of fine print.

Here are some shortcomings for annuities:

- They carry very high commissions and fees. for example, mortality and expense fee, administrative fee, contract maintenance charge, subaccount fee, state premium tax (in seven states and Puerto Rico), investment transfer fee, contingent deferred sales charge, a “surrender charge”, principal protection, inflation protection/cost-of-living adjustment, long-term care rider, lifetime income rider

- Annuities usually have a surrender period, you cannot make withdrawals during this time without paying a surrender fee. Surrender fees can be 10% or more and can decrease over many years.

- Annuities can have “riders” that provide for more benefits, but all of these come with a reduction in future income. One such benefit is as survivorship benefit.

- Loss of control of assets, and highly illiquid.

- The insurance company selling your annuity has a huge costs of doing business. They have to fund employees, executives, offices, stockholder profits etc. All of this is a cost you agree to pay when buying an annuity.

Is There an Alternative – Yes

Instead of having the insurance company build you an investment portfolio, you can build it yourself. You can start building it today, take advantage of my research if you wish.

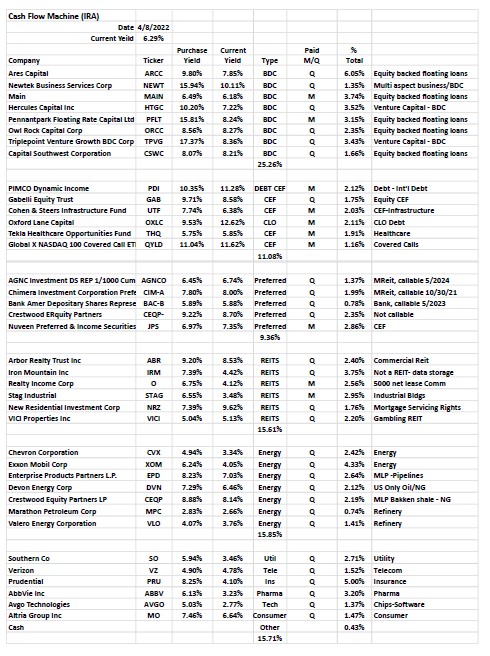

My Self-Built Annuity

Over the last 17 years I have built a diverse, safe and reliable portfolio that has held up during the 2007-8 financial market crash and the March 2020 Covid crash. The goal is to pay substantial dividends and never touch the principle. The primary focus is on generating cash – income, secondly protection of principle.

You will see I have 6 categories of investments:

- BDC, these are similar to banks that lend money to small to mid-size businesses and then help them succeed. Most of these have floating rate loans that do very well during rising interest rates

- Closed End Funds (similar to an ETF) these are specialized and include debt (bonds)

- Preferred Common Stock, these are highest priority in a company’s equity chain.

- REIT’s, these are investments in real estate, without getting a call at 2 AM to fix a toilet. Over most long terms, REIT’s actually outperform the stock market. I own Amazon warehouses, drug stores, multi-family housing, casino’s, mortgage servicing companies, etc.

- Energy, tell me a better place to invest. These include drillers, refineries, retailers and pipelines.

- Other, these are higher dividend growth opportunities.

My IRA Annuity

Download a PDF version (click here)

Benefits of My “Annuity”

- The portfolio is 100% liquid, completely under your control, no fees or restrictions.

- The principle is never reduced and can be left to future generations.

- It handles 100% of my RMD, while leaving almost 1/2 of the dividends for reinvestments.

- You can easily tweak it annually to take advantages of future trends and opportunities.

- High yielding stocks/bonds are not as volatile as general market indexes, like the DOW or S&P 500.

- The dividend yield has remained in the 6 – 61/2% range.

- My Q1 2022 dividends were 10% higher than 2021 and 12% higher than 2020 (before the pandemic). Dividend growth is a multiplier.

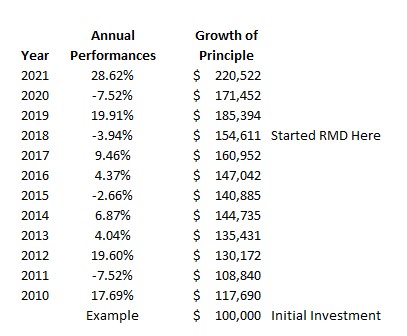

How Has it Performed?

Here is a screen shot with performance numbers from Fidelity. Over the last 10 years, after RMD’s the value of the portfolio is more than double. For example, if you initially invested $100,000 you would have gained over 2 times your investment, after taking out cash income to help live on.

Am I Against Annuities?

No, for people who completely understand what they are getting and don’t want to build their own, an annuity could be a good fit in a portfolio.