Yes, this is the cover a 1973 Money Magazine about a year after it started publishing. Easy money policies of the Fed are designed signed to generate full employment. However by the early 1970s inflation forced the Fed to raise interest rates to almost 20%! This inflation spiral lasted almost 10 years as we went into a bad recession.

Since we are a consumer driven economy, high inflation crushes our spending power, it tends to be a spiraling process. What has traditionally stopped inflation …. a RECESSION.

Here is what you should know about our current situation.

Why would we possibly have inflation? Let’s see on the Fiscal side.

- In April 2020 adults received $1,200 and dependents under 16 received $500 each!

- In January 2021 adults received $600, and dependents received $600 each.

- In March 2021 adults received $1,400, plus $1,400 per dependent, regardless of the dependent’s age.

- On top of this we added $600/week to state unemployment payments, later reduced to $300/week.

So, we had a pandemic, what was wrong with all of these payments? Mostly, these were not “needs based” payments. These were payments made by the government (adding to the whopping budget deficit) to stimulate the economy. For the most part, this was NOT to put bread on the table for most American’s. So what did America’s actually do with the money? They set up Robinhood accounts and “gambled” on crypto and meme stocks, they had their houses renovated, they bought so many cars dealers ran out. We bought so much stuff that the economy ran RED HOT! We bought so much stuff that we now have supply chain problems.

Just to clarify, there are 2 basic factors that can feed inflation., Fiscal vs Monetary policy. Monetary policy deals with the supply of money and overnight interest rates, basically the Fed. Fiscal policy is the the rest of government both spending and giving away money.

Now let’s look at the Monetary Side.

- The Fed maintains for all practical purposes a 0% funds rate. Banks and large institutions can borrow short term money for free. If it’s free, why not take advantage of it, right? True but the secret is to start turning off the money spicket at the right time. Even after clear market evidence of a super strong economy the Fed has been too slow.

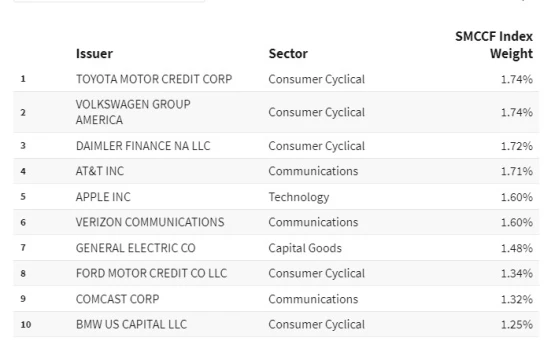

- More importantly, the Fed had been buying on the open market $120 billion/month, yes per MONTH of bonds and mortgages. This itself funneled a HUGE amount of money into the market. Leaving the Fed with a $9 trillion balance sheet! The Fed split these purchases up between $60 Billion bonds and $60 Billion mortgages … EVERY MONTH. Check out the corporate bonds the Fed was buying. Why do we need to buy bonds by Toyota, Volkswagen, Daimler and so on???? Tons and tons of money is being pumped into an already super heated economy.

- Add to all of this the mortgage backed securities MDS’s the Fed buys. They buy MBS’s to keep housing rates low, well that worked too well … housing prices instead soared!

- By the time the Fed starts to “taper” all the free money, it’s too late!

So where do we go from here?

There is good and bad inflation. Good inflation might be the Fed’s arbitrary target of 2%, assuming that the economy is growing at this or a higher rate. If we have inflation at say 3% and economic growth of only 1 1/2% we are in what’s called “stagflation”. Bad inflation is when the rate exceeds our GDP growth, as we have now. We are now experiencing BAD inflation. How do you exactly know when we have real inflation? Just check out the CPI, Consumers price Index. It’s pretty clear