If you listen to listen to conventional wisdom (I don’t) and invest a fair portion of your portfolio in bonds you’ll need to understand how to calculate the real yield, not what a broker or financial advisor can advertise.

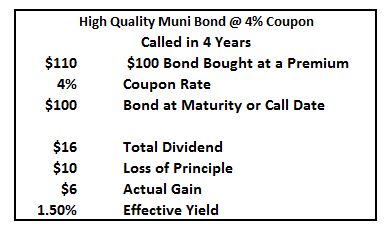

Your financial advisor suggests that you buy a high-quality Muni Bond, because of its quality you of course pay a premium, $110. This is not at all unusual. The bond coupon is 4%, your financial advisor is allowed to advertise this rate, and you’ll make $4 a year. This looks to be a pretty good yield and a safe investment. You might also notice that today Barclays Muni Bond Index yields 2.2%, you’re getting a better deal with no additional risk.

Maybe not, let’s do some math.

You have owned this bond for 4 years. Each quarterly brokerage statement shows a 4% yield and will show that you are getting your portion of the $4 annual dividend. Now the bond gets called early or matures and you get back $100. In the 4 year example your actual gain was only $6, or 1.5% yield.

Here is what you need to know.

- Brokers and financial advisors operate under an industry self-regulator called Municipal Securities Rulemaking Board and it allows them to the yield based on the bond sale price on each statement.

- A mutual fund or ETF falls under federal accounting and tax rules and will report the yield based on what you’ll actually get.

- If you buy a bond ask your broker or advisor to calculate a “yield to worst” return. If he/she won’t do some math yourself.

- Check your bond for a “callable” date, if it is still many years out it may help in your calculations.

It always pays to become educated in what you’re investing your hard earned money in.