To many people the decision on when to start taking Social Security can be a difficult decision. As we all know those that can claim Social Security may start getting benefits as early as age 62, or as late as age 70. So how do you decide when you should take yours? This actually turns out to be a Year by Year decision.

The first decision is, “Do I absolutely need the money to live on, with few other options”, if so then go ahead and start receiving benefits at age 62. However, you should also consider the idea that the longer you wait, the more you get and the difference is substantial.

Let’s look at some examples.

If you are an unmarried person, currently age 61 and trying to decide whether or not to claim Social Security at 62, you can compare claiming at 62 vs. claiming at 63. Based on a calculation the breakeven point is age 78. (If you live to age 78, you are better off having claimed at 63 than having claimed at 62.)

Using the 2011 actuarial tables from the SSA, we can calculate that for an average 62 year old male, there is a 67% probability of living to age 78. For a 62 year old female, there is a 76% probability. For most unmarried people, it makes sense to wait at least until 63, because there is a much greater than 50% probability of living to the breakeven point.

Then, at age 63, you would want to see if it makes sense to wait until 64. The breakeven point between claiming at 63 and claiming at 64 is age 76. Using the same actuarial tables, we can calculate that for an average 63 year old male, there is a 74% probability of living to age 76. For a 62 year old female, there is an 82% probability. It probably makes sense to wait another year.

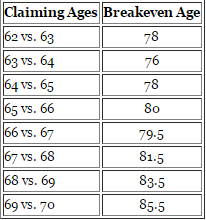

And then you would repeat this analysis every year. For somebody with a full retirement age of 66, the year-by-year breakeven ages would be as follows:

Full retirement 66

Full retirement 67

The above analysis is just a simplification, to show the general idea that the decision should be made year-by-year rather than simply asking “Should I claim at 70 or at 62?”

A real-life analysis of your situation could include a few other factors, such as:

- What would my returns be if I invested my on early-received benefits? In the above discussion I assumed a 0% real return, just a match for low inflation. This can be determined by just looking at the yields on TIPS, (the investment with a risk level most similar to that of Social Security), they are currently at or near zero, a pretty reasonable assumption. If real interest rates were higher, the breakeven points would be pushed back a little bit.

- There is a BIG difference in the actual cash payout between the years and the early claiming penalty is substantial. Keep in mind that Social Security gains a guaranteed 8% a year, tax free if you wait from “full retirement age” to age 70. That is excellent in this market.

- Tax planning can be an issue. Specifics vary from person to person, but in most cases tax planning is a point in favor of waiting to claim benefits, because of Social Security’s tax-advantaged nature.

- Spousal and survivor benefits for married couples can make a big difference.

- For anybody who is concerned about running out of money due to a very long retirement, delaying Social Security is often a good decision, even if there is a less than 50% probability that they will live to the breakeven point in question.

What should you do? If you think you are going to live into your 80”s, which has a high probability, they longer you wait, the more money you’ll have to live on.

Here is another interesting article on the real value of Social Security as if it were a bond!